Rent-seeking is any deliberate attempt to obtain rents, usually by political power, market power, influencing and using the law, or a combination of such means. Rent-seeking benefits no one, except the rent-seeker. It is a good idea to discourage rent-seeking, and some ideas about that are discussed below.

In the wonderful book The invisible hand? How market economies have emerged and declined since AD500, Bas van Bavel analyzes three examples of pre-industrial market economies: Iraq in the early Middle Ages, Italy in the high Middle Ages, and the Low Countries in the late Middle Ages and the early modern period. He analyzes that these societies thrived with dynamic and open markets, and how the growth of prosperity leads to the rise of new elites who accumulate assets, and how elites and privileged groups gradually tend to protect those assets, thus reducing dynamic and open markets. We can view this process as an increase in rent-seeking, which gradually leads to a decline of a society in the long run. With this in mind it is a good idea to pay attention to rent-seeking and to consider means to discourage it.

Katharina Pistor is the author of the book “The code of capital”. The subtitle is “How the law creates wealth and inequality”. This book describes how a simple object, an idea, or a promise to pay can be transformed into an asset that creates wealth. By doing this she explains how capital is created by lawyers.

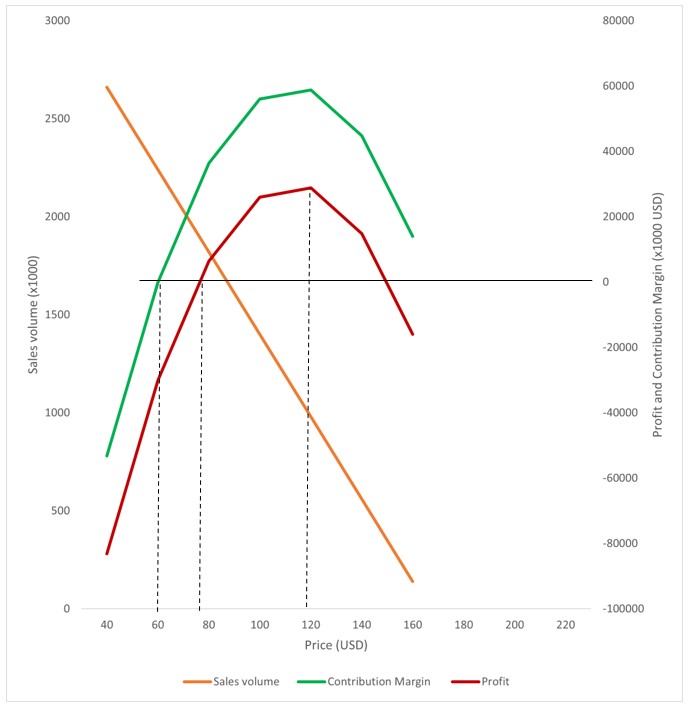

In figure 1 the contribution margin is the contribution to cover fixed costs, and is calculated as revenues minus variable costs (for the precise numbers see year-2021 in table 1 below). Many firms use the contribution margin as base for pricing because it is often difficult and rather arbitrary to allocate fixed costs among products. The dashed vertical lines in figure 1 define three important prices for the supplier. The left line (price = 60) is the ‘minimum price’ where the contribution margin is zero. The middle dashed line (price = 80) is the ‘required price’ where the contribution margin is equal to fixed costs. The third dashed line (price = 103) is the ‘maximum price’ which optimizes the contribution margin and profit. Any price above this maximum reduces profit, due to price elasticity of demand. Even a monopolist will charge this maximum price, unless the monopolist is able to reduce the price elasticity of demand, as discussed below in the section ‘Bargaining power and price elasticity of demand’.

Another way of looking at figure 1 is that the minimum price and the maximum price define the bargaining space for a supplier. An example is the price which a hotel chain can charge for a room. In January demand is often so low that the hotel chain cannot charge more than the minimum price. If even the minimum price is not feasible the hotel may close down temporarily because the price does not even cover variable costs. In the peak season or during special events (e.g. a large trade fair) the hotel chain can charge the maximum price. The average price over the year must at least equal the required price in order to be a profitable business. If not, the hotel chain will not continue for a long time, because shareholders may sell their shares, banks may cut credit lines and it is unlikely that new investors are interested.

Bargaining power and the price elasticity of supply

If supply is flexible and fully adjusts to demand the price elasticity of supply is > 1, and no supplier can increase price more than the competition. In terms of figure 1 the average price over the year will be equal to the required price. Consequently there can be no economic rents because any higher price will be driven down by competition (see the blog How to calculate rents).

To summarize: a condition for economic rents is that the price elasticity of supply < 1.

Bargaining power and price elasticity of demand

Figure 2 is based on the same numbers as figure 1, with one important difference: the price elasticity of demand is much lower in figure 2. If the price = 100 the price elasticity of demand in figure 1 equals -1.5 while it is -0.5 in figure 2.

A monopolist may charge a price of 113 USD in figure 1, while the monopolist may charge 176 USD in figure 2. As a result the maximum profit equals almost 30 million USD in figure 1 while it is 131 million USD in figure 2. Therefore it is very attractive for a monopolist to reduce the price elasticity of demand as much as possible. If the customer is unable to use another vendor without substantial switching costs this is called a vendor lock-in. Less extreme examples of methods to reduce price elasticity of demand are: product differentiation and brand name.

One example of a vendor lock-in is Apple: the closed ecosystem of Apple products makes it quite unattractive for a customer to switch to another product. Consequently Apple can charge higher prices than competitors.

The most extreme example of figure 2 is a pharmaceutical product, with a patent, and which can cure a life-threatening disease. In such a case the price elasticity of demand will be close to zero and consequently the supplier can charge an extremely high price.

Bargaining power and inflation

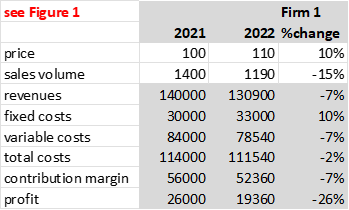

If a supplier has strong bargaining power it is easier to pass-through any cost increase, and this is illustrated by comparing firms in Table 1 and Table 2.

Table 1 Effect of 10% inflation for firm with weak bargaining power (sales volume = 3500-21*price)

Table 2 Effect of 10% inflation for firm with strong bargaining power (sales volume = 3500-12*price)

Due to inflation, both firms face an increase in their fixed and variable costs of 10%. Both firms respond by raising the sales price by 10%. However, for firm 1 the profit goes down by 26%, while for firm 2 the profit increases by 1%.

Definitions

Contribution margin: sales minus variable costs. This is the contribution to cover fixed costs.

Contribution margin ratio: (sales minus variable costs) / sales, for example (100-80)/100 = 20%. This means that 20% of sales revenues is used to cover fixed costs.

Markup: Sales / costs – 1, for example 100/80 – 1 = 1.25 – 1 = 25%. This is the percentage which is added to costs in order to calculate the sales price.

Rents are above-normal returns. This raises the question: what is a normal return?

Adam Smith described in The Wealth of Nations that the market price may deviate from a normal price, but that competition will force the market price to gravitate to the normal price. In other words: competitors will drive down prices until they allow for a normal Return On Investments (ROI), equal to the required rate of return to be able to finance investments and to survive in the long run.

A rule-of-thumb to approximate the normal ROI is the median ROI in the economy (the median ROI is better than the average because the median is not sensitive to outliers). However, this approximation is only suitable for a quick and initial estimation.

A better approach that is widely used in corporate finance and by investors is CAPM (Capital Asset Pricing Model). It is a valid approach because it includes market risks in the risk premium and excludes specific individual risks, so that the normal ROI is linked to the business cycle and not to specific factors such as the risks of individual firms. These specific risks should not be included because they can be covered by a diversified investment portfolio. The basic principle of CAPM is this distinction between risks that can be diversified and those that cannot, because they are related to the overall business cycle.

However, some types of business are more sensitive to the overall business cycle than others. In CAPM it is Beta that measures how sensitive a firm or industry is to the business cycle, see box1 below.

The CAPM approach is an approximation and not perfect, but the basic principle of distinguishing between specific individual risks and the overall risk of the business cycle is valid and important. Several attempts have been made to design more advanced methods to estimate the risk premium, but these attempts did not challenge the basic principle of CAPM and did not lead to considerably better results. For the time being it seems the best approach available.

Beta Beta does not measure the variability of a firm or industry by itself, but it does measure how this variability is related to the business cycle. If beta is 1.5 this means that the variability of a firm is the same as the overall business cycle multiplied by 1.5 . Beta is calculated as the covariance of the rate-of-return of firm i and the market-rate-of-return divided by the variance of the market-rate-of-return. The average beta of all firms is 1.

Normal ROI The required or normal ROI is calculated as: ri = rf + beta (rm – rf) where ri = required rate of return for a firm or an industry, rm is the market rate of return, and rf is the risk-free rate (commonly proxied by a 10-year government bond). In other words: if beta = 1.5 then the required rate of return is the risk-free rate + 1.5 times the difference between market rate and risk-free rate. This is the premium for the risk of greater variability than the business cycle. The market rate rm is usually based on historical annual returns of all firms. For each year I use the median of all observations because the distribution of rates of return is skewed and has outliers.

Rents can be measured as a surplus cash flow, see table1 and figure1 below.

Revenues (sales)

–

Cost of Goods Sold (COGS)

–

Selling, General & Administrative costs (SG&A)

–

Research and Development costs (R&D)

–

Investments (Capex expenses)

+

Depreciation (to adjust for the depreciation costs in COGS, because investments are fully expensed as cash flow)

–

normal Return On Investment (the return in competitive markets, which is the required return for long-term continuity of the firm)

=

surplus cash flow = rents

table1

For this calculation I use data in the operational section of the Statement of cash flows in Annual reports. The normal return on investment is discussed in the blog A normal return .

Rents in one year may be an incident, e.g. temporary scarcity due to a bad harvest or a war. It is the persistent rents which are relevant as the result of possession of scarce or exclusive assets. A proxy for persistent rents is the minimum of rents in five years. For example: if rents in the last five years were 26, 28, 22, 30, 32 % of revenues, then the minumum % in the last five years was 22%. That is: proxy for persistent rents = 22% of revenues.

Figure1 Rents as surplus cash flow

The method above is explained in detail in my paper in the Cambridge Journal of Economics, volume 47, issue 4, July 2023, https://doi.org/10.1093/cje/bead025

Adam Smith described rents as income received by landowners who “love to reap where they never sowed” (The Wealth of Nations, 1776; book I, chapter VI). However, the analysis of rents by Smith was not consistent since he described rents sometimes as surplus and sometimes as costs without a clear analysis about the difference.

It was David Ricardo (1817) who is known for the first consistent theory of rents. Ricardo made a clear distinction between revenues to owners of scarce natural assets (e.g. land) that cover the costs of the asset, from other revenues to the asset owner, which result from the bare possession of a scarce or exclusive asset. The portion of revenues that is due to ownership only is rent, while rising revenues due to investment in improvements of the asset are not rents, but rewards for costs, risks, and effort. Ricardo’s analysis, which focused on natural assets such as land and mines, was followed throughout the 19th century.

In terms of Ricardo’s theory it is important to distinguish the owner of an asset versus the producer, for example the landowner versus the farmer. Sometimes the landowner and the farmer may be one and the same person, but also in that case it is important to distinguish the producer (the farmer) and the owner of the asset (the landowner). Likewise, many pharmaceutical firms in our time produce pharmaceutical products and possess patents of these products. However, this is not always the case: some firms own pharmaceutical patents but production is by other firms who pay a license fee to the patent owner. It is important to keep in mind that in all these cases it is the owner of the asset who receives a rent while the producer receives a profit.

John Stuart Mill remained close to Ricardo’s theory, and Mill’s book Principles of Political Economy (1848) was the major textbook in the second half of the 19th century. As such it was an important book to teach the theory of rents to students of economics.

In Capital volume I and II Karl Marx did not discuss rents in any detail, but he did so extensively in volume III, which was published by Friedrich Engels in 1894 after the death of Marx. Ricardo focused on ‘extensive rent’ or ‘differential rent’: the rent that is caused by the difference between the most fertile and the least fertile soil. Ricardo assumed that farmers on the least fertile soil do not pay a rent to the landowner. The more fertile the soil, the higher the rent that the farmer has to pay to the landowner, and this is called a differential rent. In addition to differential rent Marx distinguished intensive rent (rent on land with higher investments), absolute rent (rent on the least fertile soil, due to scarcity of land), and monopoly rent.

Henry George analyzed in Progress and Poverty (1879) the causes of the increasing gap between the rich and the poor in the USA, which may be compared to the modern discussion about the 1 percent versus the 99 percent. He attacked in particular rent-seeking by land speculators, and he proposed the single land tax as solution. His book was the most popular economics book among the general public in the late 19th century.

Alfred Marshall’s book Principles of Economics (1890) was the watershed between the classical economists (Smith, Ricardo, JS Mill) and the Neoclassical economists, who dominated the economics textbooks in the 20th century. Marshall introduced the concept of quasi-rents. He analyzed rents in the manner of Ricardo as being caused by scarcity of natural resources, and he defined quasi-rents as man-made, in other words: rents in manufacturing. Marshall assumed that such rents could exist in the short run, but would gradually diminish and disappear in the long run. Unfortunately Marshall was not always precise in his definitions, but he frequently mentions “producer’s surplus or rent”, that is: as meaning the same thing. Marshall’s concept of quasi-rents did not survive him in economic theory, but his concept of producer’s surplus is still used in most economics textbooks. However, the producer’s surplus is a differential rent, it does not cover monopoly rents, market power or political power.

John Bates Clark extended Marshall’s analysis of rent and quasi-rent in his book The distribution of wealth (1899). John Bates Clark and other neoclassical economists stated that Marshall was not consistent and incomplete when he introduced quasi-rent as separate from rent, because land is just another form of capital, so there should not be any difference in the analysis of land and capital. This idea resulted in the “marginal productivity theory”: the idea that the owner of any factor of production receives a return which is in accordance to productivity. This theory has many problems (see for example the discussion in Blaug, Economic theory in retrospect) but the marginal productivity theory discusses differences in productivity, that is: differential rent, and does not include monopoly rents or market power and political power. The Neoclassical concept of marginal productivity of every factor of production has been quite influential, and as a result the concept of rents faded into the background, and was hardly discussed anymore in economics textbooks. Many students of basic economics courses have not been exposed to the concept of rents, an example is the best-selling textbook by Mankiw.

In 1933 Edward Chamberlin published ‘The theory of monopolistic competition’ and in the same year Joan Robinson published ‘The economics of imperfect competition’. Needless to say, monopolistic and imperfect competition are related to rents, and indeed both books discussed rents in a chapter or an appendix. However, as Chamberlin described, rents are a revenue and not a cost for the asset owner, but rents are a cost for the producer like any other expense. Chamberlin and Robinson focused on producers, much more so than on asset owners, and consequently rent was only a minor topic in both books. Chamberlin did add something to the analysis of rents: he analyzed in particular urban rents as ‘spatial rents’, that is: related to the distance between a shopkeeper and locations with high density of people, such as for example metro lines.

The neglect of rents as a topic in economics during the 20th century changed when Gordon Tullock published a paper in 1967 and even more so in 1974 when Anne Krueger published her famous paper about rent-seeking. Her analysis of rents was in terms of Neoclassical economics, and she coined the word ‘rent-seeking’. Rent-seeking in this school of thought is any deliberate attempt by special interest groups to influence government regulations in their favor. An example is lobbying for import tariffs to maintain high prices in the home market. Methods of rent-seeking may be lobbying, nepotism or in a rather extreme case corruption.

Joseph Schumpeter (1883-1950) rejected the focus on equilibrium in Neoclassical economics. He argued that the nature of capitalism is dynamic and not about equilibrium, and his focus was on entrepreneurs, innovation and ‘creative destruction’. Innovation can create a competitive advantage and this may generate rents as above-normal profits. Innovation rents are also known as Schumpeterian rents. However, in competitive markets innovations will diffuse and innovation rents are therefore temporary rents.

Post-Keynesian and Real-World economists reject as quite unrealistic many assumptions in Neoclassical economics, for example the U-shaped cost curves which are very familiar to economics students. Most firms are not ‘price-takers’ but ‘price-makers’: they calculate prices as the sum of costs plus any markup. Post-Keynesian price theory analyses markup in relation to market power (for example Frederick Lee, Marc Lavoie).

An important trend in the 21st century is the rise of intangible assets and Intellectual Property Rights (IPR) as a source of rents. Examples of intangible assets are patents, licenses, copyrights, and brand names. Possession of intangible assets enable the owners to have higher markups and above-normal profits which are not proportionate to their investments ( ‘to reap much more than you ever sowed’ to paraphrase Adam Smith). In the economics literature there is much discussion whether IPR and patent laws protect innovation or incentivise rent-seeking, see for example Jaffe and Lerner (2011), Innovation and it discontents: how our broken patent system is endangering innovation and progress and what to do about it. There is similar ongoing debate about whether occupational licenses protect quality or protect rent-seeking, see for example Lindsey and Teles (2017), The conquered economy.

Summary: the state of rent theory

The analysis of rents by Ricardo in 1817 was limited to natural resource assets, in particular land rent, with a focus on ‘differential rents’: rents related to the difference between fertile land and marginal land (where rents are zero because there is no surplus). After Ricardo the analysis was extended with various kinds of ‘monopolistic rents’, and with ‘non-natural rents’ which are not related to natural resources, but which are related to intangible (non-physical) assets. All extensions of Ricardo’s theory of rents have one common denominator: rents are the result of scarce or exclusive assets which reduce the flexibility of supply to match demand, and consequently increase the price above the level in competitive markets.

Rents exist in human history for thousands of years. The origin of rents is the possession of land, and until the industrial revolution the possession of scarce land was the main source of rents. In our time possession of oil and gas are the most important source of natural resource rents. However, land rents are still relevant, and urban land rents are nowadays a major determinant of house prices.

After the industrial revolution the rise of monopolies was an important cause of rents, for example the steel and railroad monopolies in the USA in late 19th century. In our modern time such old-fashioned monopolies have declined in importance, instead it is the big platforms on the Internet, the big tech firms, and the big pharmaceutical firms that have replaced the old monopolies.

In the 21st century we see a decline of tangible investments such as machines and buildings, and on the other hand, the importance of intangible (non-physical) investments and assets has increased very much, for example the increase in the number and importance of patents.

The blog A theory of Rents discusses the history of rents in terms of the theories by famous economists.